March 2026: Iran Conflict Meets Private Credit Strains: Stagflation Risks Rising

The Middle East Escalation: Regime Change, Not Disarmament

Let’s start with Iran. The U.S. and Israeli military operations in Iran reflect something far more ambitious than financial markets initially priced in: a desire for regime change, not disarming a nuclear weapons program. That’s a materially bigger goal—and a bigger potential shock—than the market consensus seemed to anticipate on Friday.

Iran’s response has been to attack U.S. military installations and civilian targets across the broader Middle East, transforming what might have been a trilateral dispute into a regional conflict with potentially longer duration and bigger scale/footprint.

The Straits of Hormuz effectively are closed, which, if sustained, will cause significant stress on commodity markets (negative supply shock raises oil prices; negative demand shock reduces prices for agricultural commodities). However, many in commodities markets believe oil prices stay around $80 as they expect the conflict to be short-lived.

The consensus outlook on the duration and scale of the conflict risks being too benign.

- On conflict duration, the consensus assumes a desire for a quick win. Iran’s Supreme Leader Ayatollah Khamenei has been killed in the strikes—a development that, while significant, does not mean the underlying conflict will be easily resolved. Iran has succession plans, and a half-century of state-sponsored oppression does not crumble in a few days. However, President Trump has indicated a willingness to allow the conflict to go for “four weeks or so.” At the same time, Israel has achieved its multi-decade dream of support from a US administration to affect Iran regime change. A quick resolution affects less change and does not serve Israel’s purpose.

- On conflict scale, Iran’s remaining leadership both has thousands of drones and ballistic missiles and now views itself in a fight to the death. Iran is widening the conflict to the Gulf States, presumably so that they will lobby the US to stop the war. Most salient to oil and financial market impacts, Iran’s strategy risks damage to the region’s oil and liquified natural gas (LNG) assets. Saudi Arabia’s estimated spare capacity is ~2-2.5 million bbl/d. Prolonged bombardment in the region risks damage to Gulf State oil and LNG assets. Iran’s oil production totals ~3-3.5 million bpd. US ground forces in 2003 were needed to secure Iraq’s oil fields to stop anticipated widespread burning. Recall that Iraq set fire to Kuwait’s oil fields in the 1991 Gulf War. It took eight months to extinguish the 1991 well-head fires in Kuwait and the recovery of Kuwait’s oil production took several more years. Will US ground troops be needed again to protect Iran’s oil producing assets? The Administration repeatedly has not ruled out ground forces.

In terms of the bond market, this is where the analogy to past crises matters. The 1979–1980 Iran crisis and the 1990–1991 Gulf War unfolded in starkly different macroeconomic and military contexts, and markets responded very differently.

In 1979–1980, the U.S. inflation was already elevated when the Iran crisis happened and the higher oil prices that accompanied it poured gasoline on an existing fire. Treasury yields surged to around 15% as inflation and Fed Chair Volcker tightening dominated; oil prices more than doubled and stayed elevated for years; gold shot to nearly $800–850 per ounce; and the S&P 500 delivered weak real returns as stagflation, high rates, and ultimately a recession battered US equities.

By contrast, the 1990–1991 Gulf War occurred in a disinflationary environment. Oil spiked briefly but normalized quickly once supply security was assured. Treasury yields actually fell on the invasion, driven by flight-to-safety and growth concerns. The S&P 500 bottomed before the shooting even started and then rallied sharply as victory appeared assured.

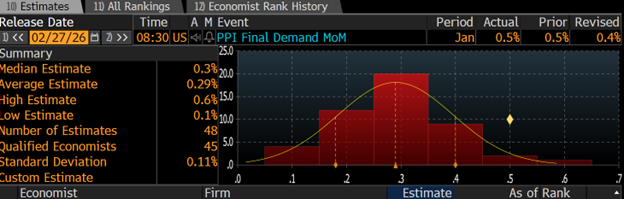

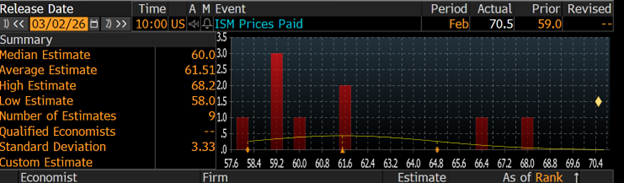

In my view, the Iran conflict’s scale and macro setup resembles 1979–1980 far more than 1991. In my February column I outlined why I believed even prior to the military action against Iran that inflation risks were skewed to remaining meaningfully above target. Friday’s PPI came in hot as did Monday’s ISM Prices Paid.

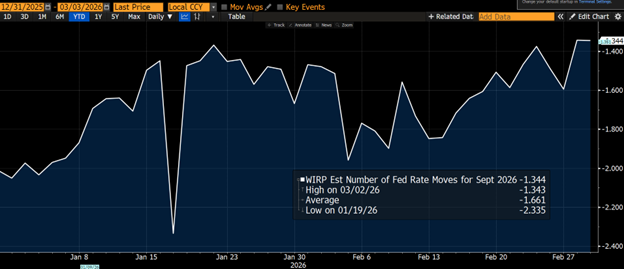

My view is that as energy markets reprice still higher that Treasury yields will rise further. At this juncture, Treasury yields have risen both due to expectations of higher inflation (one-year TIPS inflation breakevens look priced for $100 oil/~4% CPI) and a repricing of the Fed’s policy path to price out some rate cuts.

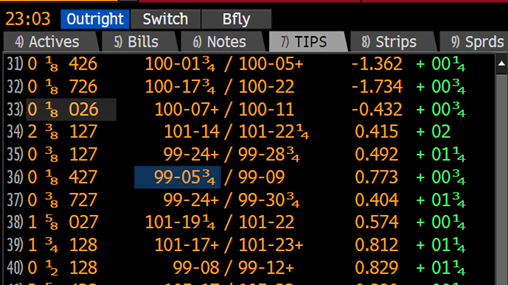

As can be observed below, front dated inflation protected securities (TIPS) are trading at negative real yields out to October 2026. Because inflation accrues to TIPS with a 3-month lag that implies bond market participants anticipate energy shocks to elevate inflation into the summer of 2026, well beyond a week or two.

Yes, US Shale — But Everyone Still Has a Problem

There’s one bright spot: the U.S. economy has shale as a bit buffer from extreme oil price spikes. But don’t mistake US production for unequivocally good news. While the US is an oil exporter and has expanded its domestic production the US still consumes ~7-8 million bbl/d more than it produces. An oil price shock will hit the US less hard than 1979-1980, but it will certainly still land a painful blow. However, given their greater dependence on imports, China, the EU, UK and Japan will feel stagflationary impacts far more directly if this conflict drags on—higher inflation and lower growth simultaneously. $100+ oil would be synchronized global stagflationary shock.

Energy is necessary to the economy and, as result, elevated energy prices can lead to recessions. Higher prices act as an inflationary shock that forces deleveraging elsewhere in the global financial system. For example, to pay for more expensive oil, some countries may be forced to sell dollar assets, like Treasuries, causing yields to rise further. Additionally, higher oil prices reduce the real value of the budget deficit and associated stimulus. Higher energy prices and inflation also require that banks lend more in nominal terms to maintain the same real value of credit in the economy. Policymakers often fail to understand how inflation tightens financial conditions until it is too late. In this way, as global energy prices rise so will recession probabilities.

The Private Credit Complication

Now we get to the truly uncomfortable part: the private credit market has spent the last few years becoming untethered from fundamentals in ways that are about to be stress-tested. In 2023, when U.S. banks faced deposit flight and liquidity stress due to monetary tightening, private credit benefited from an inverted and then flattening yield curve.

Non-bank financial institutions (NDFIs) could originate floating-rate assets, obtain credit ratings, and issue debt in public markets—all while borrowing long-term at attractive term premia because the yield curve was inverted. It was, briefly, a favorable financial environment for private credit balance-sheet management.

But that calculus has deteriorated sharply. Short-term interest rates have been coming down and banking sector liquidity has tightened due to prior Fed QT. The phase of private credit growth driven by favorable financial conditions now looks to be over. Ironically, more Fed rate cuts would lower the value of private credit’s assets and worsen its balance-sheet position further. And that is before we factor in inflation shocks from Iran starting to put upward pressure on long-dated Treasury yields which makes private credit’s funding more challenging.

Software, Spreads, and the Leverage Trap

In 1979-1980, software actually was one of the best performing sectors of the US stock market.[1] Rising credit spreads in the software sector have received considerable attention, but I suspect the real story is less about fundamental challenges from AI and more about what private credit’s generous underwriting has wrought: massive overinvestment and inefficiency in software firms even as investors pivot towards U.S. companies producing tangible goods and manufacturing. An inflation induced tightening of financial conditions could serve as a tipping point for the sector.

[1] See table on granular performance of US sectors on pg 29 of Journal of Portfolio Management, “The Best Strategies for Inflationary Times,” Aug 2021.

So private credit is experiencing strain from both emerging credit risk in SaaS companies and from deteriorating financing conditions.

What Does This Mean for Banks?

It is well known that banks’ exposures to private credit have grown materially since the GFC.

It is crucial that banks deeply understand NDFIs’ underwriting, credit monitoring, and workout processes. The 20% risk weight that regulators have assigned to NDFI exposures under the risk-based capital standard is, frankly, insufficient if the economics of these exposures truly resemble leveraged or subprime lending. Bank management teams and boards need to recognize the actual economics and ensure they have enough capital behind these credits. There is no free lunch.

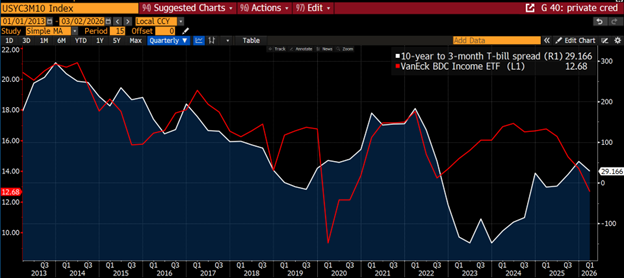

Asset values in private markets are described as both “high and stable”— yet the share price of private credit firms have fallen back to levels not seen since earlier years, suggesting potential credit downgrades ahead.

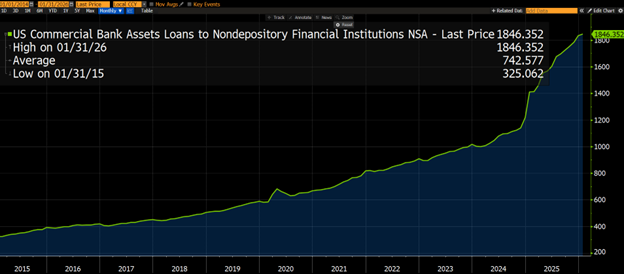

Banks need a full understanding not just of their on-balance-sheet lending to private credit but also off-balance-sheet exposure—the credit lines they’ve extended that could be drawn down. Undrawn US bank credit to NDFIs is estimated to stand at over $900 billion. When private credit asset origination begins to back up on their balance sheets and the CLO and other distribution channels become clogged, banks should expect higher drawdowns. Recent drives to place private credit assets with high-net-worth retail investors and into ETFs could be a signal that the distribution channel is already becoming a concern. Moreover, allegations of fraud—First Brands, Tricolor, and late last week MFS—affecting private credit have exposed weaknesses in collateral due diligence. Private credit firms tried to take significant collateral in their credit extensions, but their due diligence has demonstrated notable gaps. Worse, private credit may seek to subordinate an obligor’s other creditors, including banks and bondholders. Banks need to carefully evaluate and potentially guard against these risks.

The Convergence: Energy Shock Meets Financial Fragility

So here we are. The private credit market previously had been running on favorable financial conditions—an inverted curve, ample Fed liquidity, and low credit losses—for the better part of the post-COVID period. That era is over. Simultaneously, geopolitical tensions are rising globally, energy prices, inflation pressures and long-dated Treasury yields are also rising.

Banks need to:

- Model energy and commodity scenarios for credit and rates. Geopolitical shocks to energy markets in the Gulf could be outsized and longer-lasting than the consensus expects. Stress-test exposures to energy-intensive industries, to agricultural commodity producers who may be negatively affected if shipping in the Gulf remains challenged and to firms whose leverage was predicated on stable energy. I recommend reviewing the 1979-1980 Iranian revolution US sector performance in this publication on pg 29. Assuming a $50 per barrel increase in the price of oil translates into ~100 bps more inflation is a reasonable starting point. Bringing that inflation estimate into a Taylor rule which would seem to imply a pricing out of Fed rate cuts into Q4 2026 based on current consensus estimates for employment.

- Stress test for stagflation which can result in banks facing credit, interest rate and liquidity stress simultaneously.

- Higher energy prices imply greater demand for dollars in the global financial system. Ensure on-balance sheet liquidity is adequate and test contingent funding plans. Indeed, I spent a bit of time last week increasing the liquidity of my own portfolio.

- Reassess private credit relationships carefully. Review loan documentation for strength of material adverse change and other covenants. Understand NBFIs’ underwriting standards and collateral positions.

- Recognize that private credit economics may resemble leveraged lending or subprime more than the risk weights suggest. Capital ratios should reflect true economic risk, not regulatory minimums.

- Prepare for higher private credit drawdowns and associated liquidity stress as asset distribution channels become congested and balance sheets tighten.

- Evaluate any CLO exposure and review the degree of over-collateralization and assumed correlation in the securitization.

Honestly, I would welcome being wrong about scope and duration of the Iran conflict and stagflation risks. But hope is not a strategy – so I wish Treasury Talk readers focus and thoughtful analysis and contingency preparation in the days ahead!

[1] See table on granular performance of US sectors on pg 29 of Journal of Portfolio Management, “The Best Strategies for Inflationary Times,” Aug 2021.